Headquarters

EnergyCAP, LLC

360 Discovery Drive

Boalsburg, PA 16827

Denver, CO

Suite 500

5445 DTC Parkway

Greenwood Village, CO 80111

Dublin, Ireland

Unit F, The Digital Court, Rainsford Street,

Dublin 8, D08 R2YP, Ireland

Phone: 877.327.3702

Fax: 719.623.0577

California’s climate accountability laws, SB 261 and SB 253, set new expectations for how companies doing business in the state disclose climate risk and greenhouse gas emissions. SB 261 requires biennial climate-related financial risk reporting, while SB 253 requires annual disclosure of scopes 1, 2, and 3 emissions.

If you operate in California and meet the set revenue thresholds, these laws are likely to apply to you, making data readiness and governance a near-term priority. Read our complete guide to learn what these regulations mean for your business, when and how to submit your GHG reports, and the best ways to collect the data.

Key Takeaways

Together, SB 261 and SB 253 create two obligations for large companies that do business in California: publish a climate-risk report every two years (SB 261) and disclose annual greenhouse gas emissions across scopes 1, 2, and 3 (SB 253).

If your annual revenue exceeds $500 million (SB 261) or $1 billion (SB 253), these laws are likely to apply, even if your headquarters are outside the state of California. Building supplier engagement, normalizing utility data, and establishing audit trails will shorten your close and reduce verification friction later.

A practical path is to centralize utility bills and emissions factors in a single system of record, such as EnergyCAP Utility Management with Carbon Hub, to streamline data collection, conversions to scopes 1–3, and evidence for assurance. Support your process with a modern sustainability reporting platform.

CARB’s rulemaking signals ongoing administrative fees and program infrastructure, so budgeting for data collection, assurance, and internal review will be part of annual compliance. Assign clear ownership across finance, sustainability, procurement, and IT to keep filings accurate, consistent, and on time.

Pro Tip: Want deeper context on timing, scope, and assurance? Watch our webinar on decoding California’s climate disclosure laws.

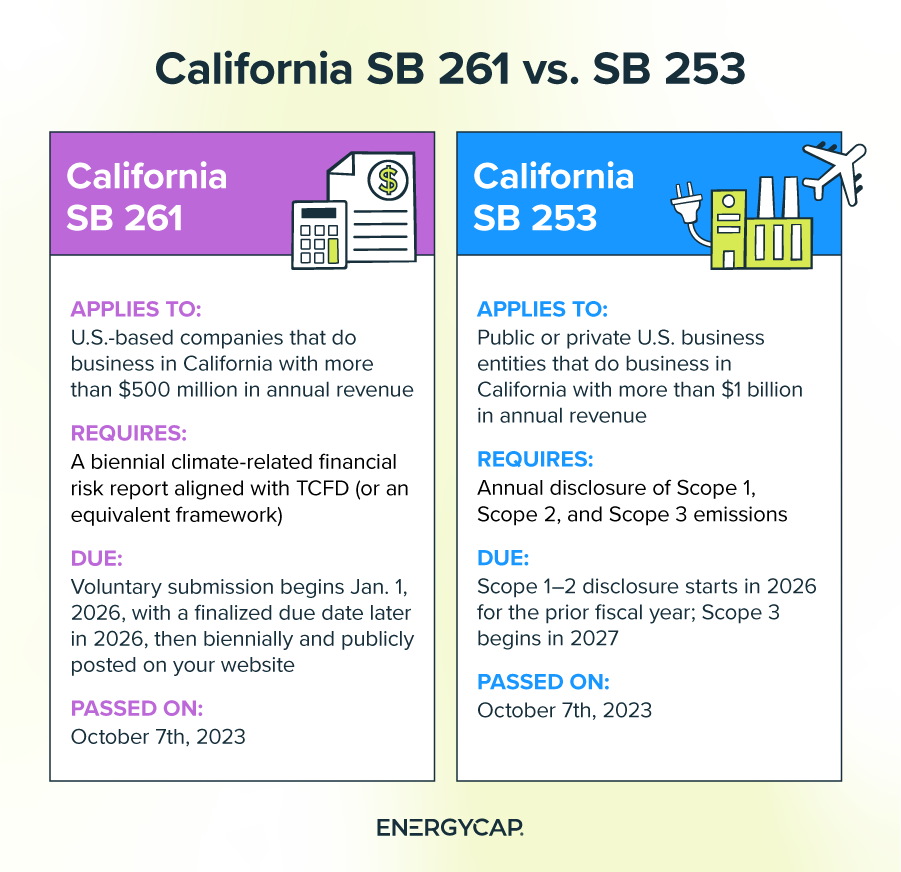

Who it applies to: U.S. companies that do business in California with more than $500 million in annual revenue (prior fiscal year)

Passed on: Oct. 7, 2023

SB 261 requires a biennial climate-related financial risk report aligned with TCFD (or an equivalent framework). The report must disclose material climate-related financial risks and the measures your company is taking to reduce and adapt to those risks, and you must publicly post it on your website. Parent-level consolidation is allowed.

CARB will assess an annual program fee and may seek administrative penalties for non-filing or inadequate reports, capped at $50,000 per reporting year. For current implementation materials, see CARB’s SB 261 checklist.

Who it applies to: Public or private U.S. business entities that do business in California with more than $1 billion in annual revenue (prior fiscal year)

Passed on: Oct. 7, 2023

SB 253, California’s Climate Corporate Data Accountability Act, requires annual disclosure of Scope 1 and Scope 2 emissions starting in 2026 (for the prior fiscal year) and Scope 3 beginning in 2027.

Disclosures must follow the Greenhouse Gas Protocol and be submitted to a CARB-designated emissions reporting organization, which will host a public digital platform.

Third-party assurance ratchets from limited assurance on scopes 1–2 beginning in 2026 to reasonable assurance in 2030; CARB may require limited assurance for scope 3 beginning in 2030.

The program includes annual administrative fees and allows penalties up to $500,000 per reporting year for non-filing or other violations. For scope and eligibility details, see CARB’s Greenhouse Gas Reporting programs page.

California’s climate disclosure push built on earlier legislative attempts, including SB 260 (2021–2022), which set the stage for economy-wide corporate transparency but did not pass. Lawmakers reintroduced the concept in 2023 as SB 253 (Sen. Scott Wiener) and paired it with SB 261 (Sen. Henry Stern) to address both emissions disclosure and climate-related financial risk.

Governor Gavin Newsom signed both bills on Oct. 7, 2023, directing the California Air Resources Board (CARB) to write implementing regulations and indicating that follow-up “cleanup” legislation would be pursued to fine-tune timing and program mechanics. CARB established a program page covering both laws and began rulemaking and stakeholder outreach soon after.

In 2024, the Legislature enacted SB 219 to amend elements of SB 253 and SB 261, most notably extending CARB’s deadline to adopt emissions reporting regulations from Jan. 1, 2025, to July 1, 2025, clarifying parent-level consolidation, and refining administrative mechanics. These updates are now part of California’s Climate Accountability package and inform current compliance planning.

California set near-term timelines for both laws. Most organizations should work backward from their fiscal year-end to align data gathering, internal review, and assurance.

For a forward look at budgets, staffing, and tech choices tied to these timelines, explore our 2026 energy management outlook.

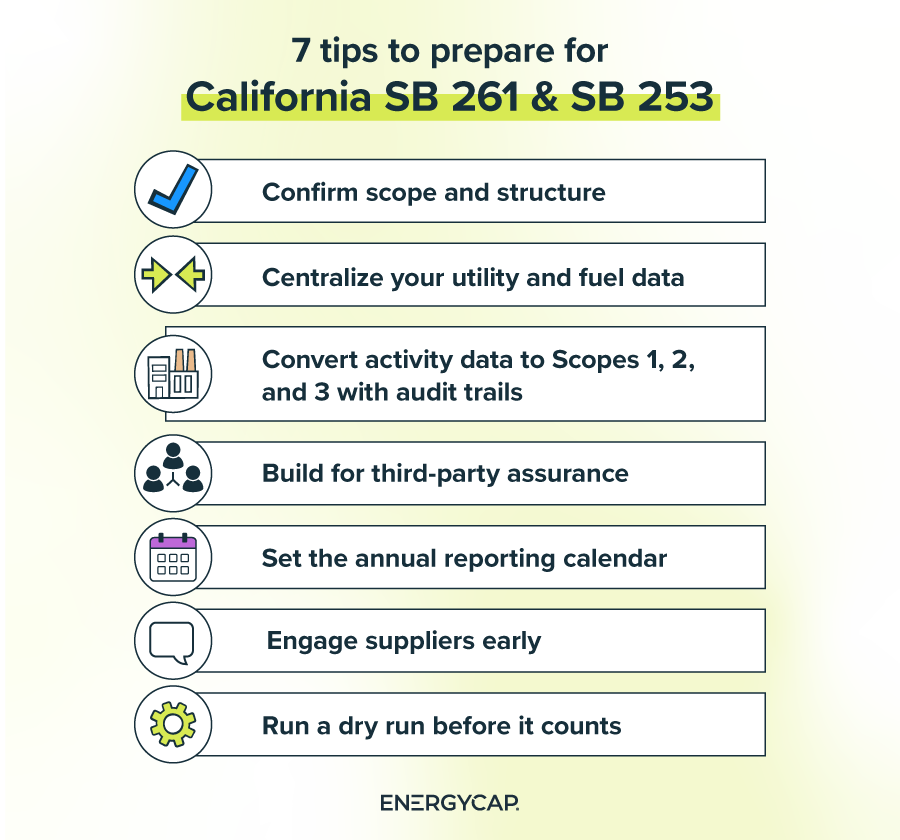

California’s climate laws are data-heavy and deadline-driven, but preparation does not have to be complicated.

Decide whether to report at the parent level, then create a single source of truth for bills, meters, and fuel so you can calculate scopes 1–3, maintain audit trails, and move smoothly into third-party assurance.

From there, lock in an annual calendar that lines up with your fiscal year, clarify who owns what, and practice your process before the first filing.

Our steps below keep it practical for your team:

SB 261 and SB 253 raise the bar on climate-risk reporting and GHG disclosure. If you centralize utility data, standardize calculations, and build audit-ready workflows now, you’ll be ready for third-party assurance and smoother submissions.

EnergyCAP Utility Management, Bill CAPture, Carbon Hub, and Smart Analytics work together to pull bills into a single system, convert activities into Scope 1, 2, and3 emissions, maintain evidence, and surface issues before filing.

Request an EnergyCAP demo to get a walkthrough, timelines aligned to your fiscal year, and a clear plan to prepare your next reporting cycle.

Both laws authorize CARB to charge annual administrative fees to cover program costs. SB 253 requires a reporting entity to pay an annual fee to recover CARB’s implementation costs. SB 261 likewise requires covered entities to pay an annual fee, adjusted over time as needed.

For SB 253, companies will file to a CARB-designated emissions reporting organization (or to CARB) that will host a public digital platform for disclosures.

For SB 261, companies must post the climate-risk report on their own website; CARB provides a public docket where entities must submit a link to that posting.

SB 253: Administrative penalties for non-filing, late filing, or other failures are capped at $500,000 per reporting year; between 2027–2030, penalties tied to Scope 3 apply only for non-filing, and good-faith Scope 3 misstatements are not penalized.

SB 261: Administrative penalties are capped at $50,000 per reporting year. In both cases, CARB must consider factors like past compliance and good-faith efforts.

SB 253: Entities with more than $1 billion in total annual revenue that do business in California.

SB 261: Entities with more than $500 million in total annual revenue that do business in California. Applicability is determined using the prior fiscal year’s revenue.

SB 253 requires annual disclosure of Scope 1, Scope 2, and Scope 3 emissions, measured in line with the Greenhouse Gas Protocol.

SB 261 is a climate-related financial risk disclosure; it does not require a separate emissions inventory, though companies may reference emissions in the narrative.

SB 253: Independent assurance is required on emissions disclosures with limited assurance for Scopes 1–2 starting in 2026, moving to reasonable assurance in 2030; CARB may establish assurance for Scope 3 by 2027, with limited assurance on Scope 3 beginning in 2030.

SB 261: The statute does not mandate assurance on the climate-risk report.