Headquarters

EnergyCAP, LLC

360 Discovery Drive

Boalsburg, PA 16827

Denver, CO

Suite 500

5445 DTC Parkway

Greenwood Village, CO 80111

Dublin, Ireland

Unit F, The Digital Court, Rainsford Street,

Dublin 8, D08 R2YP, Ireland

Phone: 877.327.3702

Fax: 719.623.0577

The fine print is already written. California’s SB253 requires Scope 1 and 2 emissions disclosures beginning August 2026. New York’s S9072A mandates statewide energy benchmarking. New York City’s LL97 imposes building emissions caps with penalties already in effect. Boston’s BERDO applies to large commercial buildings. At least a dozen more states are drafting similar legislation right now.

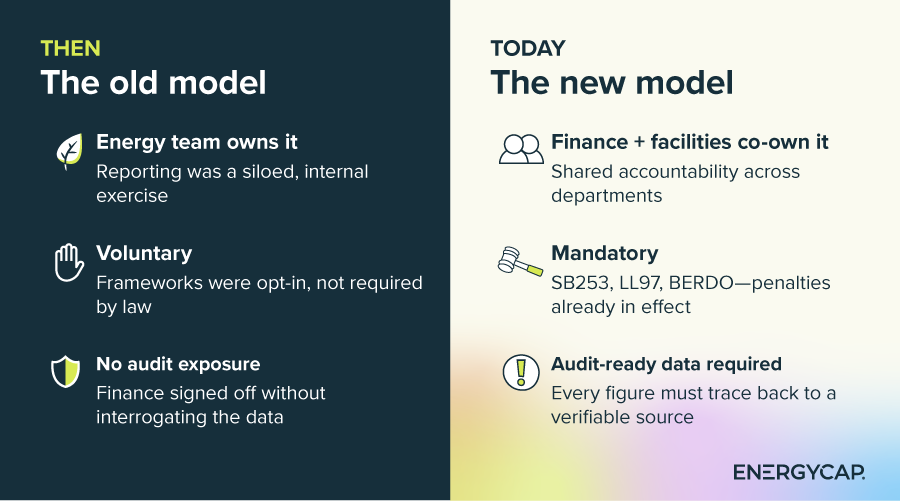

Sustainability reporting used to be a quarterly exercise the energy team owned. Now it is a financial disclosure with audit exposure, and facilities directors and finance leaders share the accountability, not just the energy team.

That shift changes what sustainability reporting software needs to do. This post explains what to look for, what the compliance deadlines mean for your team, and how to evaluate whether your current data can hold up under audit. For the full state-by-state mandate picture, see our post on energy benchmarking compliance laws.

For most organizations, sustainability reporting lived in a silo: the energy manager ran the numbers, submitted to ENERGY STAR®, and filed the report. Finance signed off without deeply interrogating the data.

That era is ending. SB253—California’s Climate Corporate Data Accountability Act—requires large companies doing business in California to disclose Scope 1 and 2 emissions beginning August 2026. New York’s S9072A extends energy benchmarking requirements statewide. NYC’s LL97 is already imposing per-ton penalties on buildings that exceed their emissions caps. Boston’s BERDO applies similar rules to large commercial buildings.

The common thread: these are no longer voluntary reporting frameworks. They carry penalty exposure, audit risk, and the same data lineage requirements that apply to financial reporting. Facilities directors who own the buildings and finance leaders who own the budget are both on the hook.

The question sustainability reporting software has to answer is no longer ‘can you produce a number?’ It is ‘can you show your work?’

Sustainability reporting software tracks an organization’s greenhouse gas emissions—primarily Scope 1 and Scope 2—and produces the documentation needed for regulatory filings, voluntary disclosures, and internal carbon accounting.

Scope 1 emissions are direct: natural gas combustion, fleet fuel, on-site generators. Scope 2 emissions are indirect: purchased electricity, steam, chilled water, and district heating. Both fall under SB 253’s August 2026 disclosure requirements, and both require source data that traces back to a verifiable utility record or meter read.

Modern sustainability reporting platforms pull utility data through three primary channels: direct utility feeds (EDI), meter integrations, and ENERGY STAR® Portfolio Manager®. From there, the platform applies emission factors—location-based Scope 2 uses regional grid emission factors (eGRID); market-based Scope 2 uses supplier-specific or residual-mix factors—and produces a GHG inventory.

EnergyCAP Emissions produces raw GHG inventory data: Scope 1 and Scope 2 totals by site, by account, by period, with emission factors documented and traceable to the source invoice. Customers then format that inventory for each specific disclosure mandate or their jurisdiction’s required template. That is the honest answer: the platform produces audit-ready data; the formatting for each mandate is the customer’s step.

For a deeper look at tracking emissions over time, see our post on emissions tracking software.

Nearly half of organizations don’t yet have the data and insights they need to proactively manage utility programs—let alone produce audit-ready emissions disclosures. That’s not a failure of effort. It’s a structural problem: utility data is fragmented across vendor portals, spreadsheets, and paper bills, and the teams responsible for it are lean.

42% of organizations run utility programs reactively or with inconsistent automation.

According to the EnergyCAP State of Utilities 2026 report, 70% of energy management teams have six or fewer people. Bandwidth is a top-three blocker across all respondents. And 40% of external respondents cite ‘need more data’ as their number one barrier to hitting energy management goals, ahead of budget and staffing.

Consider what quarterly Scope 2 reporting looks like without a platform: a facilities team pulling meter reads from 200 sites, cross-referencing against invoices, applying emission factors manually, version-controlling spreadsheets across multiple reviewers, and then hoping the numbers hold up if an auditor asks to trace a figure back to its source. It is the kind of workflow that produces emissions estimates rather than emissions data.

That distinction matters enormously under the new mandates. For more on the utility data foundation underneath this problem, see our post on utility data management.

The word ‘investment-grade’ gets used loosely in sustainability circles. In facilities and finance, it means something specific: data that a bank, auditor, or regulator could examine and trace back to its source without gaps.

For emissions reporting, investment-grade means: verified at the meter, traceable to the source invoice, documented emission factors with methodology noted (location-based vs. market-based for Scope 2), complete audit trails showing who changed what and when, and version control that lets you reconstruct any prior filing.

Most spreadsheet-based and generic ESG-tool approaches break at the data lineage step. The number gets produced, but the chain from meter read to invoice to emission factor to final disclosure figure is not maintained in a way that survives audit scrutiny.

EnergyCAP’s position in this category comes from four decades of utility data management: the platform was built around the invoice and the meter, not bolted on afterward. That history is what makes the resulting emissions data defensible—not as a sustainability claim, but as a financial one. When your facilities team submits a Scope 2 figure to a regulator, it should trace back to a verifiable utility account the same way a capital expenditure traces back to an invoice.

If you’re evaluating options ahead of a compliance deadline, these are the criteria that separate platforms built for audit exposure from those that produce estimates:

Can the platform pull utility data directly from your accounts, not just accept a spreadsheet upload? Look for direct utility feeds (EDI), meter integrations, and ENERGY STAR® Portfolio Manager® connectivity. ENERGY STAR® integration specifically eliminates double entry for benchmarking submissions—the data flows once and appears in both places.

The platform should support both location-based and market-based Scope 2 calculation methodologies. Location-based uses regional grid emission factors (eGRID in the US); market-based uses supplier-specific or residual-mix factors. SB253 and the GHG Protocol require both. Confirm which emission factor databases the platform uses and how frequently they are updated.

This is the criterion most buyers underweight. An audit-ready platform maintains a complete record of every data change: who changed it, when, and what the previous value was. When a regulator or external auditor asks you to verify a figure from a prior filing, you should be able to pull that record without reconstructing it from memory or backups.

Sustainability reporting under state mandates is not a configure-once situation. Regulations change, emission factors are updated annually, and filing requirements vary by jurisdiction. A platform backed by people who understand utility data (not just software) matters when the requirements shift.

Finance teams need emissions data to flow into the same reporting workflows as other operating costs. Confirm whether the platform can export in formats your ERP or financial reporting system accepts, and whether it maintains the data lineage in that export.

Emissions addresses each of these criteria: automated data ingestion from utility accounts and ENERGY STAR, location-based and market-based Scope 2 calculation, complete audit trails, and four decades of utility expertise behind the platform.

The organizations facing the most immediate compliance pressure are those operating under multiple overlapping mandates: a university system with campuses in California and New York, a hospital network with large commercial buildings in NYC, a government agency subject to both BERDO and state benchmarking laws.

EnergyCAP is used by hospitals, universities, and government agencies across multiple jurisdictions—organizations that manage large, complex building portfolios and now face overlapping state and local emissions mandates. Most customers report saving more than 10% on utility costs year over year, and the same data quality that drives those savings is what makes emissions reporting defensible.

If your next compliance deadline is 12 months or fewer away, here is a practical starting point:

If you want to see how EnergyCAP handles this process, request a demo or explore Emissions to see the Scope 1 and 2 GHG inventory capabilities.

Sustainability reporting software tracks an organization’s Scope 1 and Scope 2 greenhouse gas emissions and produces the documentation needed for regulatory filings, voluntary disclosures, and internal carbon accounting. The key differentiator from generic ESG tools is data lineage: the ability to trace every reported figure back to a verifiable utility record or meter read, which is what audit-ready disclosure actually requires.

Not exactly. Sustainability reporting software focuses on emissions and energy disclosure specifically: Scope 1, 2, and sometimes 3 reporting tied to utility data. ESG software is the broader category that includes social and governance reporting alongside environmental. For a facilities or finance leader focused on compliance mandates like SB253 or LL97, sustainability reporting software is usually the more specific fit — the problem is utility data and emissions calculation, not social metrics or board governance.

Scope 1 emissions are direct: sources the organization owns or controls, such as natural gas combustion on-site, fleet fuel, and backup generators. Scope 2 emissions are indirect: purchased electricity, steam, chilled water, and district heating. Both fall under SB253’s August 2026 disclosure requirements, and both require source data traceable to an invoice or meter record.

Nearly all states have either statewide, or city-specific, benchmarking and building performance laws on the books, with many more states drafting similar legislation. For the full state-by-state picture, see our post on energy benchmarking compliance laws.

Most modern platforms pull utility data through three main channels: direct utility feeds (EDI), meter integrations, and ENERGY STAR Portfolio Manager. EnergyCAP’s specific advantage is four decades of utility data normalization — the platform was built around the invoice and the meter, which is what makes the resulting emissions data traceable and defensible under audit.

Lead with the data lineage question: can the platform trace every reported emissions figure back to its source invoice or meter read? After that: Scope 2 calculation methodology (location-based and market-based both available), audit trail depth, ENERGY STAR integration, and services support as regulations evolve. EnergyCAP is built around these criteria — the data quality that underpins 10%+ annual utility savings is the same quality that makes emissions disclosures defensible.